Purpose and scope

The purpose of this policy is to manage the risk of any significant disruption to service levels by holding an appropriate amount in reserves [1] that allows for a managed response to any unforeseen reduction in income or additional expenditure. This policy informs the way SALC manages it cash, liquid assets, debt and assists with future planning. It is designed to contribute to balancing the needs of current and future beneficiaries, provide stakeholders with assurances that SALC is well managed and that it has, where appropriate, a strategy for building up and managing reserves.

[1]

The term “reserves” is used to describe that

part of SALC’s income that is freely available for operational purposes, not

subject to commitments, planned expenditure and spending limits.

Responsibilities

The SALC Board owns this policy and will review annually and update as necessary. On a day-to-day basis all members of the team shall be responsible for following procedures and processes and highlighting any updates or amendments necessary to ensure continual improvement.

Risk-based approach

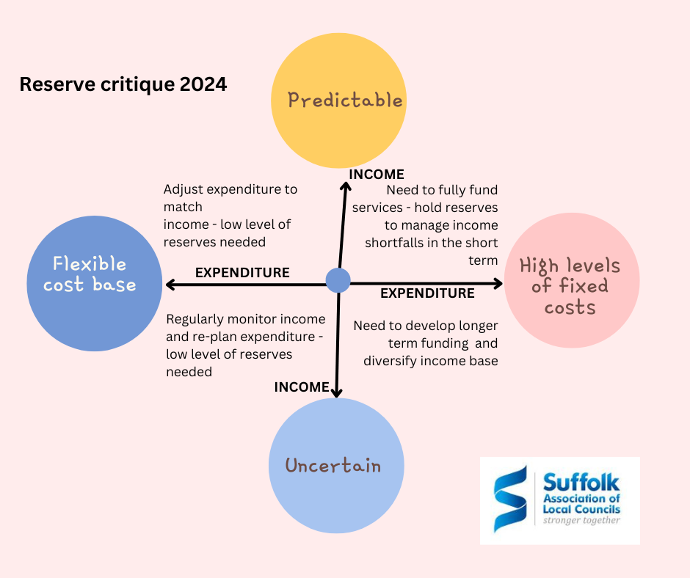

SALC have approached the calculation of their reserves using a risk-based approach (see reserve critique below). Due to a low level of fixed assets an income-based bias has been adopted in order to evaluate the impact of that loss. The risks identified are:

-

an unforeseen drop in income either from subscriptions or grant funding and/or

-

unbudgeted increases in expenditure

Calculation for reserves

The SALC Board have set the target range for an appropriate amount of free [1] reserves at £150,000, representing circa 50% of annual income and expenditure so as to manage risks in the short-term until longer-term solutions are established. This is deemed an appropriate figure to ensure sufficient flexibility in the context of operational requirements for an organisation of the size and complexity of SALC based on the current budget.

[1] “Free reserves” includes both cash and investments which are immediately available.

Types of reserves

SALC has two types of reserves:

-

General reserves (including staff) are funds which do not have any restrictions as to their use and used to smooth the impact of uneven cashflows, offset the budget requirement if necessary or can be held in case of unexpected events or emergencies.

-

Earmarked reserves are funds which can be used to cover specific items such as investments in systems, infrastructure, policy development, specialist support, invest to save initiatives such as employing new staff to develop and grow services.

Managing and reporting

Reserves shall not be used to fund ongoing expenditure but can

be used to meet short-term funding gaps.

Any earmarked reserves that have been used for short-term funding gaps

must be replenished as soon as possible.

However, those earmarked reserves used to meet a specific liability do not need to be replenished, having served the purpose for which they were originally established.

SALC’s financial risk assessment is part of the budgeting and year-end accounting procedures and identifies planned and unplanned expenditure for which they are held.

Reserves are recorded on SALC’s financial management system and

form part of their monthly bank reconciliation procedures. On a quarterly basis the SALC Board review

income and expenditure reports as part of budget monitoring procedures which

includes an update on reserves.

Changes to this policy

This is a controlled document and is the responsibility of the SALC Board and is reviewed annually.